You submit an invoice at 9:07 a.m. By 9:09 a.m., software has read the document, scored your customer’s credit, priced the advance, and queued the wire. The money hits your account before lunch. No phone tag. No PDF email chains. No week-long underwriting review.

That is what AI accounts receivable financing actually looks like in 2026 — and it is already funding thousands of small businesses every day. But there is a lot of hype around “AI-powered” lending, so you need to know what is real, what is marketing, and what it means for your cash flow.

What AI Actually Does in AR Financing (And What It Doesn’t)

Strip away the buzzwords and AI in receivables financing boils down to software — specifically machine learning (ML) models, which are programs that learn patterns from historical data and then apply those patterns to new situations. In AR financing, those models do four concrete jobs:

- Invoice valuation: Predicting how likely an invoice is to be paid, and when.

- Customer credit scoring: Evaluating the creditworthiness of your debtors in seconds using live business data.

- Fraud detection: Flagging duplicate invoices, altered documents, and suspicious debtor patterns.

- Predictive cash flow: Forecasting when each invoice will actually pay — not just when it’s due.

What AI does not do: replace the fundamentals. A factor still needs creditworthy customers, clean invoices, and no existing liens on your receivables. AI makes decisions faster and cheaper — it does not eliminate them.

Faster Approvals and Automated Invoice Valuation

The biggest change you will feel with AI accounts receivable financing is speed. What used to take a human underwriter a week — reading invoices, verifying customers, checking documents against bank statements — now takes software 30 seconds.

Modern lenders use optical character recognition (OCR) to extract every field from an invoice PDF, then cross-reference it against your accounting system, your bank deposits, and your customer’s payment history. An API (application programming interface — a way for two software systems to talk to each other) then pulls real-time credit data on your customer from providers like Dun & Bradstreet or Experian Business.

Why This Matters

In 2022, a $25,000 invoice from a new customer often took 3-5 business days to fund. In 2026, the same invoice from a pre-vetted customer can fund in under 4 hours — sometimes under 30 minutes. For a deeper playbook on getting funded fast, read how to speed up your AR financing approval.

What to Expect From a Modern 2026 Application

A best-in-class AR financing application in 2026 should include:

- Secure upload of invoices and accounts receivable aging report (drag and drop, no faxing)

- Read-only bank data connection (via Plaid or similar) — no emailing PDF statements

- Direct integration with your accounting software (QuickBooks, NetSuite, Xero)

- Same-day decisions for clean files; 24-48 hour setup at the outside

- Online dashboard showing advance status, reserves, and fees in real time

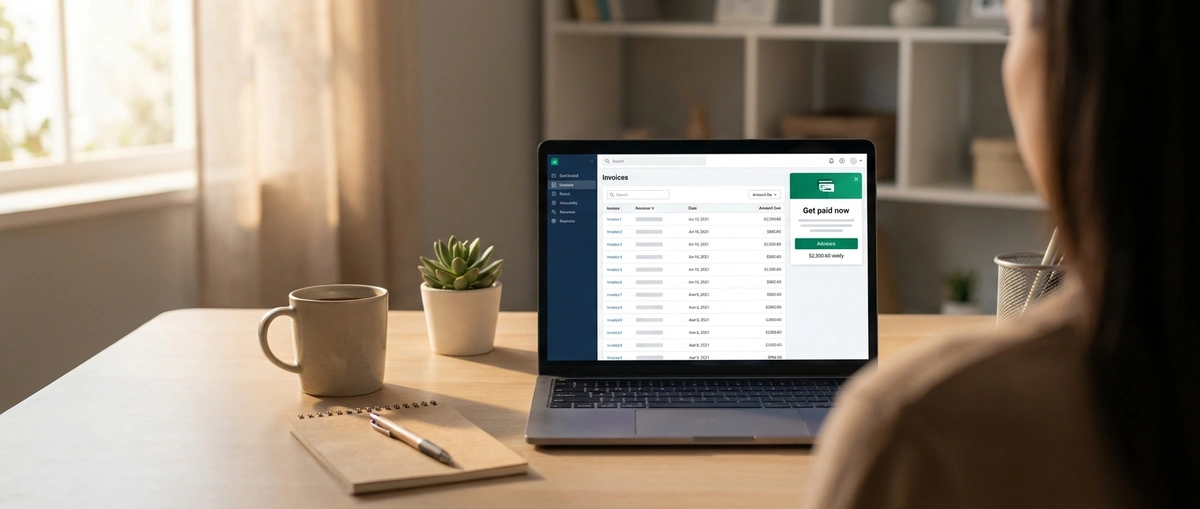

Embedded Finance: AR Financing Inside Your Accounting Software

Embedded finance is a fintech term for financial products that live inside another tool. Instead of going to a factor’s website, filling out a form, and emailing invoices, you click a button inside QuickBooks that says “Get paid now.” The financing happens without ever leaving your accounting software.

This is happening across every major accounting platform in 2026. QuickBooks, NetSuite, Xero, and FreshBooks have all rolled out AR financing partners — or their own in-house products — directly inside the app. Your invoice data, customer history, and bank connections are already there, so the lender doesn’t need to ask for anything you haven’t already typed in once.

For a small business owner, this collapses friction dramatically. No data re-entry. No lost documents. No “where is that statement from March?” No learning a new platform just to get funded. The integration is the point.

Real-Time Credit Assessment and Fraud Detection

Traditional factoring checks your customer’s credit once — at onboarding. Modern AI-driven factors monitor continuously. If one of your debtors starts paying other suppliers 20 days late, the system sees it the same week.

Detect

ML models pull payment data, public filings, and news sources daily. Changes in debtor behavior trigger alerts.

Score

Each debtor gets a rolling risk score. Strong scores unlock higher advance rates; weak scores trigger review — not auto-decline.

Act

Fraud models flag duplicate invoices, shell debtors, and altered documents before the advance is wired. Clean invoices fund faster.

For you as the business owner, this means better rates on your good customers and fewer surprises. Industry research from Deloitte’s 2026 banking outlook notes that AI-driven underwriting has cut small business lending decision costs by more than 40% over the past three years.

Predictive Cash Flow: Knowing Your Liquidity Before It Hits

This is the quietly game-changing piece. Modern AR financing platforms no longer just advance money against invoices — they forecast when every one of your invoices will actually be paid, and build a rolling 13-week cash flow projection automatically.

The model learns each debtor’s real payment behavior. A net-30 customer who historically pays on day 42 doesn’t get forecasted as day 30 — the software knows better. That means you can plan payroll, inventory purchases, and hiring decisions against real liquidity, not invoice dates that no one actually respects.

Cash flow used to be a guessing game. AI turns it into a weather forecast — not perfect, but good enough to decide when to carry an umbrella.

Hype vs. Real: Sorting the Marketing From the Useful

Not everything labeled “AI-powered” is useful. Here is the honest split between what technology actually delivers in AI accounts receivable financing and what is mostly marketing:

| Real and Useful | Hype or Overstated |

|---|---|

| Automated invoice OCR and validation | “Fully autonomous lending with no human review” |

| Real-time debtor credit checks via API | “Guaranteed approval powered by AI” |

| Embedded financing inside accounting software | “AI that eliminates all requirements” |

| Continuous risk monitoring and fraud detection | “Instant approval on any invoice, any customer” |

| Predictive cash flow forecasting | “Rates unaffected by customer credit quality” |

Be skeptical of any lender who won’t explain in plain English how their “AI” works. Good technology teams will show you the dashboard, explain the models, and tell you exactly what still gets reviewed by a person. You still need the same core fundamentals covered in our guide on invoice financing requirements that guarantee approval.

Why AI Accounts Receivable Financing Matters Most for Small Businesses

Key Takeaway

AI in AR financing isn’t about replacing humans — it’s about lowering the cost of making a lending decision. And when decisions get cheaper, lenders can profitably fund businesses they used to turn away.

For years, small businesses heard the same excuse from banks: “You’re too small for us to underwrite profitably.” That was true when underwriting cost $2,500 a file. It is not true when software does 80% of the work in three minutes.

The practical result: a $500K-revenue business with $40K in monthly invoices can now access the same diligence tools, near-real-time advances, and embedded integrations that used to be reserved for mid-market companies with CFO teams. The same technology that funded a Fortune 500’s receivables book in 2020 is now powering funding for a three-person staffing agency in 2026. To understand the full mechanics from application to cash, see our blueprint on how AR financing works.

The Bottom Line

AI accounts receivable financing is not a replacement for the fundamentals — creditworthy customers, clean invoices, and clear terms still matter most. What changes is everything around those fundamentals: speed, access, transparency, and cost.

When you pick an AR financing partner in 2026, ask three questions. Do they integrate with your accounting software? Can they explain their underwriting in plain English? Do they show you real-time status on every advance? If yes to all three, you are looking at modern infrastructure. If not, you are looking at a 2015 factor with a new logo.

Get Funded on Modern AR Financing Infrastructure

Stop waiting a week for an underwriter to open your email. LineFlowAR uses modern automation to fund clean invoices in hours, not days — with transparent pricing and real-time status on every advance.